Gold firms post-Fed hold, trims losses from Trump comments on Iran

- Gold rebounds after dropping to $3,362 on Trump’s openness to Iran talks.

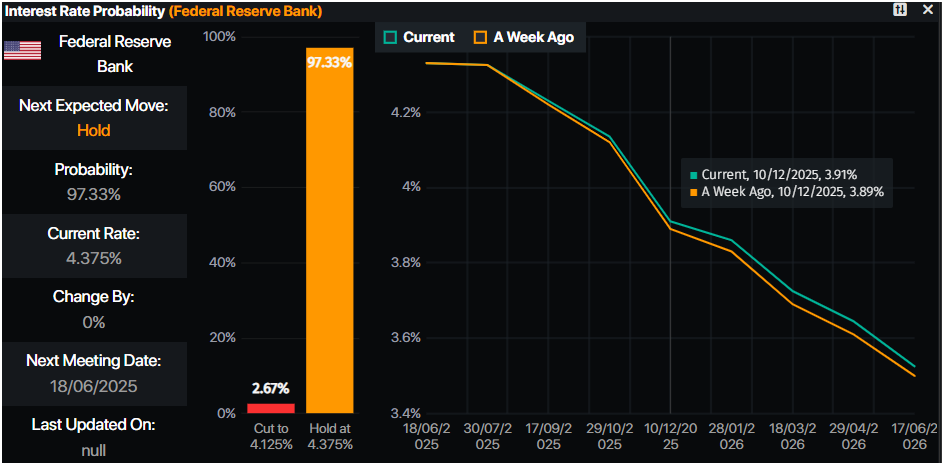

- Fed holds rates; projections point to two cuts and slower 2025 growth.

- Weak US jobless and housing data support bullion amid global uncertainty.

Gold prices show minimal gains as the Asian session begins, following the Fed’s decision to maintain rates, while indicating they are still considering two rate cuts. Meanwhile, US President Donald Trump’s comments on Iran triggered a pullback towards a weekly low of $3,362, before settling at around current levels. The XAU/USD trades at $3,375, up 0.19%.

On Wednesday, the Fed maintained rates as expected and updated its economic projections for the United States (US). The medians suggest that Gross Domestic Product (GDP) would be lower than the March forecasts, while the unemployment rate would rise slightly. Inflation would likely end at around the 3% threshold, while the Federal funds rate forecasts indicate that policymakers are eyeing 50 basis points of easing.

Meanwhile, US President Donald Trump at a press conference said that if Iran wants to come to the White House, he said, “I may do that.”

At the same time, Fed Chair Jerome Powell stood to its mildly neutral-hawkish stance, reaffirming that monetary policy is “well positioned to respond” to external shocks like tariffs or geopolitical risks.

Aside from this, a raft of US economic data revealed that the labor market has continued to ease as the number of Americans filing for unemployment benefits rose as expected. Housing data disappoints investors.

Daily digest market movers: Gold price tumble deep below $3,400 post-Fed

- The Federal Reserve left the target range for the fed funds rate unchanged at 4.25%–4.50%, reaffirming that the US economy continues to expand at a solid pace, with labor market conditions remaining strong. The FOMC reiterated its commitment to monitoring risks to both sides of its dual mandate and confirmed plans to continue reducing its holdings of Treasuries.

- Updated projections from the Summary of Economic Projections (SEP) showed a slight downgrade in the 2025 GDP growth outlook to 1.4% from 1.7% in March. The unemployment rate forecast was revised up to 4.5% from 4.4%, while the core PCE inflation projection rose to 3.1% from 2.8%.

- At his press conference, Powell said, “The effects of tariffs will depend on the level,” adding that “Increases this year will likely weigh on economic activity and push up inflation.” He said that “As long as have the kind of labor market we have and inflation coming down, right thing to do is hold rates.”

- US Initial Jobless Claims rose by 245,000 for the week ending June 14, matching market expectations. Continuing Claims, used to soften the rate of change in the weekly print, fell 6,000 to a seasonally adjusted 1.945 million during the week ending June 7.

- Meanwhile, the housing sector showed signs of cooling. May Housing Starts fell to 1.256 million units, marking a 9.8% MoM drop from April’s 1.392 million. Building Permits also edged lower, down 2% MoM to an annual rate of 1.393 million from 1.422 million previously.

- The US Dollar Index (DXY), which tracks the performance of the Dollar against six major currencies, tumbles 0.18% to 98.64.

- US Treasury yields continued to drop, as the US 10-year Treasury yield edged down two basis points (bps) to 4.367%. US real yields followed suit, falling almost five bps to 2.057%.

- Money markets suggest that traders are pricing in 46 basis points of easing toward the end of the year, according to Prime Market Terminal data.

Source: Prime Market Terminal

XAU/USD technical outlook: Gold price hovers near $3,400, awaiting a fresh catalyst

Gold price remains upwardly biased, but printing back-to-back Dojis indicates traders awaiting the Fed decision. The Relative Strength Index (RSI) is also flat but bullish. Hence, if Powell and other governors turn dovish, expect a rally past $3,400 and beyond.

In that outcome, the next key resistance would be the $3,450 mark and the record high of $3,500 in the near term. Conversely, if XAU/USD tumbles below the day’s low of $3,370, the pullback could extend toward the $3,350 mark and possibly lower. The following key support levels would be the 50-day Simple Moving Average (SMA) at $3,301, followed by the April 3 high-turned-support at $3,167.

Risk sentiment FAQs

In the world of financial jargon the two widely used terms “risk-on” and “risk off'' refer to the level of risk that investors are willing to stomach during the period referenced. In a “risk-on” market, investors are optimistic about the future and more willing to buy risky assets. In a “risk-off” market investors start to ‘play it safe’ because they are worried about the future, and therefore buy less risky assets that are more certain of bringing a return, even if it is relatively modest.

Typically, during periods of “risk-on”, stock markets will rise, most commodities – except Gold – will also gain in value, since they benefit from a positive growth outlook. The currencies of nations that are heavy commodity exporters strengthen because of increased demand, and Cryptocurrencies rise. In a “risk-off” market, Bonds go up – especially major government Bonds – Gold shines, and safe-haven currencies such as the Japanese Yen, Swiss Franc and US Dollar all benefit.

The Australian Dollar (AUD), the Canadian Dollar (CAD), the New Zealand Dollar (NZD) and minor FX like the Ruble (RUB) and the South African Rand (ZAR), all tend to rise in markets that are “risk-on”. This is because the economies of these currencies are heavily reliant on commodity exports for growth, and commodities tend to rise in price during risk-on periods. This is because investors foresee greater demand for raw materials in the future due to heightened economic activity.

The major currencies that tend to rise during periods of “risk-off” are the US Dollar (USD), the Japanese Yen (JPY) and the Swiss Franc (CHF). The US Dollar, because it is the world’s reserve currency, and because in times of crisis investors buy US government debt, which is seen as safe because the largest economy in the world is unlikely to default. The Yen, from increased demand for Japanese government bonds, because a high proportion are held by domestic investors who are unlikely to dump them – even in a crisis. The Swiss Franc, because strict Swiss banking laws offer investors enhanced capital protection.

Copy Link

Copy Link Share on Facebook

Share on Facebook Share on X

Share on X Share by Email

Share by Email