Gold holds firm below $3,400 as strong Dollar defies global turmoil

- Gold trades at $3,380 as stronger US Dollar overshadows safe-haven demand.

- Trump mulls joining Israel in strikes on Iran, fueling geopolitical anxiety.

- Fed expected to hold rates steady; Dot Plot revisions may hint at fewer 2025 cuts.

Gold prices retreated below the $3,400 level on Tuesday despite deteriorating risk appetite as overall US Dollar (USD) strength drove the yellow metal lower. Nevertheless, the escalation of the Israel–Iran conflict would likely underpin the precious metal due to its safe-haven appeal. At the time of writing, XAU/USD trades at $3,380, down 0.05%.

Market mood is downbeat, but Bullion has failed to rally as the US Dollar stages a comeback. The US Dollar Index (DXY), which tracks the performance of the Dollar against six major currencies, is up 0.46% at 98.58.

On Monday, US President Donald Trump abruptly exited the G7 meeting in Canada due to developments in the Middle East. He posted on his social network that “Everyone should immediately evacuate Tehran,” in a clear signal of an escalation of the conflict that erupted last Friday.

Earlier news sources revealed that Trump is evaluating joining Israel to attack Iran. As of writing, Walla News/Axios, citing senior US officials, said that Trump is seriously considering attacking Iran and is holding a crucial meeting with his advisers.

Even though sentiment remains the main driver, economic data in the United States (US) was weaker. US Retail Sales in May were mixed with monthly figures contracting, while in the 12 months to May they rose. Industrial Production, revealed by the Federal Reserve (Fed), shrank in May.

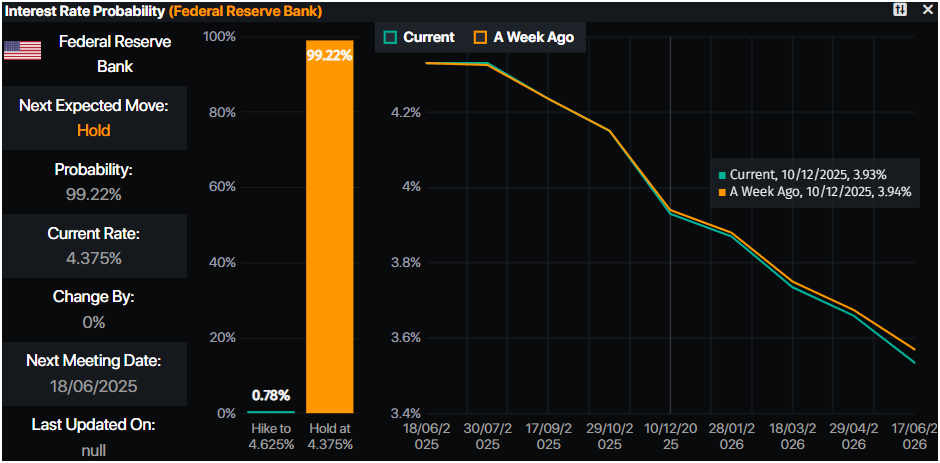

Traders are bracing for the Fed’s decision. Fed Chair Jerome Powell and other Fed governors began their “conclave” and are expected to hold rates unchanged. It is worth noting that policymakers would update their economic projections, which would signal the monetary policy path toward the second half of 2025.

Win Thin, Global Head of Market Strategy at BBH, revealed that he expects a dovish tilt by the Fed but noted that “we see some risks of a hawkish shift in the Dot Plots, as it would take only two officials to move from two cuts to one to get a similar move in the 2025 Dot.”

Daily digest market movers: Gold stays flat as rising geopolitical risks loom

- US Retail Sales fell sharply in May, dragged down by a notable decline in automobile purchases. The headline figure dropped by 0.9% MoM, underperforming expectations for a -0.7% decrease. On a YoY basis, sales climbed 3.3%, decelerating from April’s robust 5% gain.

- Meanwhile, US Industrial Production slipped by 0.2% in May, marking the second decline in three months. The data missed market forecasts for a modest 0.1% increase, signaling weakness in the manufacturing sector.

- The latest inflation reports in the US warrant further easing by the Fed. Any dovish hints by the US central bank could boost Gold prospects as the non-yielding metal fares well in lower interest rate environments.

- The World Gold Council published its central bank survey published annually, revealing that 95% of the 73 respondents expect an increase in Gold reserves over the next 12 months.

- US Treasury yields are diving as the US 10-year Treasury yield edges down nearly five-a-half basis points (bps) to 4.403%. US real yields followed suit, falling almost five bps to 2.103%.

- Money markets suggest that traders are pricing in 44 bps of easing toward the end of the year, according to Prime Market Terminal data.

Source: Prime Market Terminal

XAU/USD technical outlook: Gold price consolidates near $3,400 ahead of FOMC meeting

Gold price uptrend remains intact as price action remains constructive, achieving a successive series of higher highs and higher lows. Any retracements could be seen as an opportunity to buy the dip, as momentum measured by the Relative Strength Index (RSI) remains bullish.

With that said, the XAU/USD first resistance would be the $3,400 mark, followed by $3,450 and the record high of $3,500 in the near term.

Conversely, if XAU/USD stays below $3,400, the pullback could extend toward the $3,350 mark and possibly lower. The following key support levels would be the 50-day Simple Moving Average (SMA) at $3,293, followed by the April 3 high-turned-support at $3,167.

Risk sentiment FAQs

In the world of financial jargon the two widely used terms “risk-on” and “risk off'' refer to the level of risk that investors are willing to stomach during the period referenced. In a “risk-on” market, investors are optimistic about the future and more willing to buy risky assets. In a “risk-off” market investors start to ‘play it safe’ because they are worried about the future, and therefore buy less risky assets that are more certain of bringing a return, even if it is relatively modest.

Typically, during periods of “risk-on”, stock markets will rise, most commodities – except Gold – will also gain in value, since they benefit from a positive growth outlook. The currencies of nations that are heavy commodity exporters strengthen because of increased demand, and Cryptocurrencies rise. In a “risk-off” market, Bonds go up – especially major government Bonds – Gold shines, and safe-haven currencies such as the Japanese Yen, Swiss Franc and US Dollar all benefit.

The Australian Dollar (AUD), the Canadian Dollar (CAD), the New Zealand Dollar (NZD) and minor FX like the Ruble (RUB) and the South African Rand (ZAR), all tend to rise in markets that are “risk-on”. This is because the economies of these currencies are heavily reliant on commodity exports for growth, and commodities tend to rise in price during risk-on periods. This is because investors foresee greater demand for raw materials in the future due to heightened economic activity.

The major currencies that tend to rise during periods of “risk-off” are the US Dollar (USD), the Japanese Yen (JPY) and the Swiss Franc (CHF). The US Dollar, because it is the world’s reserve currency, and because in times of crisis investors buy US government debt, which is seen as safe because the largest economy in the world is unlikely to default. The Yen, from increased demand for Japanese government bonds, because a high proportion are held by domestic investors who are unlikely to dump them – even in a crisis. The Swiss Franc, because strict Swiss banking laws offer investors enhanced capital protection.

Copy Link

Copy Link Share on Facebook

Share on Facebook Share on X

Share on X Share by Email

Share by Email